Putting Your Home's Equity To Work with a HELOC

Your Guide To Home Equity Lines of Credit

HELOC (pronounced hee-lock) is an abbreviation for Home Equity Line of Credit. It’s a type of loan that allows homeowners to borrow money against the equity in their home.

It functions similar to a credit card, in that you can borrow any amount you need, up to your pre-set limit, and you only pay interest on what you borrow. However, a Home Equity Line of Credit typically has a much lower interest rate than a credit card because your home is used as collateral.

A HELOC can be a great way to pay for a variety of expenses. We’ll explore common uses for a HELOC later in this article. First, let’s get to know the lingo.

To understand how a Home Equity Line of Credit works, it’s helpful to get familiar with the meaning of some phrases and abbreviations related to this type of loan. Here are the basics:

Equity - Equity is the market value of your home, minus what is owed on the property. Equity is gained from:

For example, if you owe $90,000 on your home and it is appraised for $100,000, you have $10,000 in home equity.

LTV (Loan-to-value) ratio - This is a measure that compares the amount of your mortgage loan with the appraised value of the property. To put it another way, the LTV ratio tells you how much a property is worth in the market compared with how much is owed on the mortgage loan.

For example, if you owe $90,000 on your mortgage and it appraises at $100,000, that’s an LTV ratio of 90%. Your LTV ratio will change as you pay down your principal, and/or as the housing market fluctuates.

Why does LTV matter?

LTV can be used to determine what types of home equity loans a borrower qualifies for, as well as the cost and fees related to obtaining a home equity loan or line of credit.

Most home equity lenders have a maximum LTV limit. Your individual LTV limit can also be determined by your credit history or your state of residence.

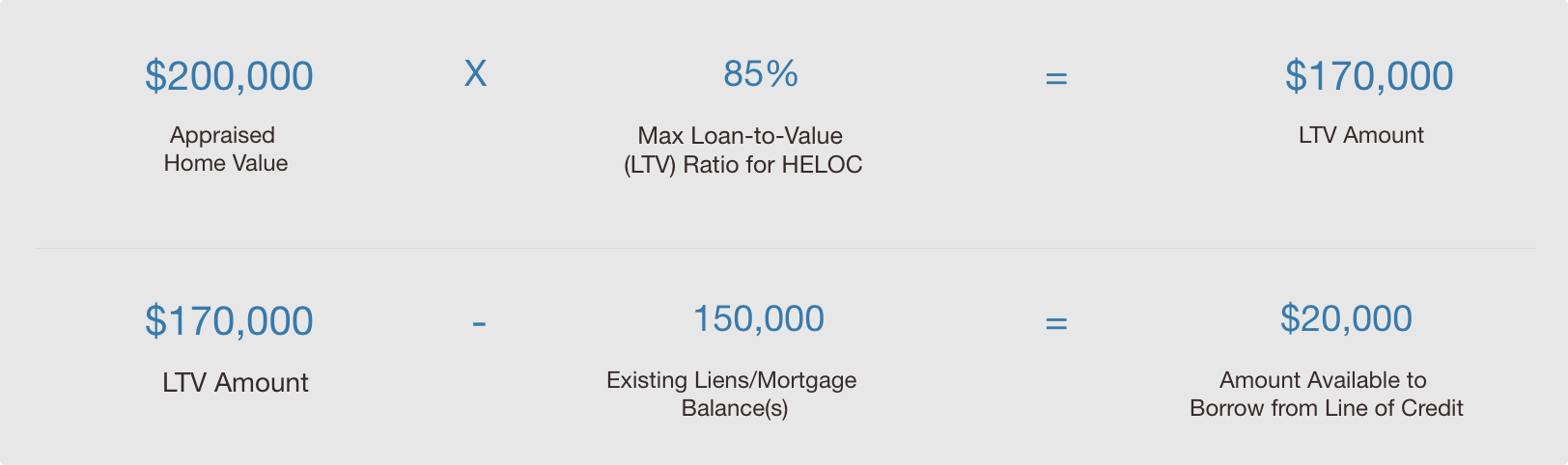

For example, if the bank has an LTV of up to 85%. This means you can borrow up to 85% of your home’s value, minus what is owed on the property.

Take a look at the math below to get an idea of how much you could borrow from your home’s equity. Be sure to try values lower than 85% so you can get an idea of how much you can borrow if the bank determines a lower LTV.

Fixed Rate - This means the rate is fixed, or stays the same, for a period of time. You may see phrases like, “12 Month Fixed Introductory Rate” or similar. This means that any advance you make during that 12 month period will accrue interest at the same rate. And after the 12 month period is over, your balance and any new advances will accrue interest at the variable rate as stated in your loan documents.

Variable Rate - A variable rate is named for how it behaves. This kind of rate can change to be higher or lower, and is usually based on the Wall Street Journal Prime Rate, plus a margin. Your credit history may be used to help the bank determine the margin. Usually, the better the credit history, the lower the margin.

Because variable rates change, you may see your monthly payment amount change. This can be tricky to manage with automatic debit, which is why borrowers are encouraged to enroll on Digital Banking. Having access to your loan details online means you’ll have a convenient way to see your payment each month.

Amortization - This is a big word that, in the simplest terms, refers to a period in which a debt is paid off or reduced by regular payments.

We do not charge any application fees, appraisal fees, or closing costs for a Home Equity Line of Credit. However, there is a $50 annual fee, which is waived for the first year of your line of credit.

Now that you know the lingo, let’s talk about the process of getting a Home Equity Line of Credit with us.

The easiest way to start an application is to apply online through our website. You can complete your application, upload your documents, and receive the final decision all through a secure online portal. Best of all, there are no application fees with us.

Before applying online, you'll need to gather some information. Locate the most recent pay stubs for all applicants, as well as Social Security number(s) and other personal information. You'll also need information about your home.

Applying online is quick and easy. Once your application is submitted, we’ll let you know if we need additional documentation to be uploaded to the portal. We’ll also help arrange an appraisal for your home. There is no charge for the appraisal. Once the appraisal is complete and our team has finished reviewing everything, we’ll contact you with a decision. From there, we’ll schedule a time to meet with you to close on your new loan.

When your loan is approved, be sure to enroll in Digital Banking so you can manage your loan, make advances on your line of credit, and make payments.

This is where the big benefits come in! Your HELOC can be used to pay for just about anything. Just keep in mind that your home is the collateral, so make sure you’re borrowing responsibly.

Some common uses for a Home Equity Line of Credit are:

Your line of credit can also be used for things like financing a family vacation, putting in a pool, or buying a car. Again, keep in mind that your home is the collateral. Be sure to weigh the financial pros and cons for any project or expense you want to fund with your HELOC.

A HELOC typically has an “advancing period,” sometimes referred to as a “draw period,” as well as a “repayment period.” During the advancing period, you can make any number of advances on your line of credit, up to your pre-set limit. For example, if you need to advance $1,000 for a home repair and then two weeks later your dishwasher needs to be replaced, you can make another advance for the amount you need to purchase a new dishwasher. Plus, any amount you pay down becomes available for you to borrow again.

After the advancing period, your loan goes into a 15 year repayment period. During this time, advances cannot be made. However, you can always reapply for a new Home Equity Line of Credit. And you can take advantage of SmartLock to lock a portion of your balance into a fixed-rate loan. We’ll explain this in detail a bit later.

With us, you can make an advance by transferring money to your Bank account using our online banking website or our mobile app. You can also use paper checks, which can request by calling ExpressBank. You can also visit a banking center to get cash from your line of credit.

SmartLock

We offer a feature called SmartLockSM that allows you to lock portions of your HELOC balance into fixed-rate loans during the advancing and repayment periods. As you pay down the balance of your SmartLock, the funds again become

available for you to borrow.

Locking your balance with this feature does not mean it will be locked at the current variable rate. It means that your balance will be locked using terms and rates similar to a Home Equity Loan. If you’re interested in locking a portion of your balance, the best place to start is by talking with a banker. They can advise you about the terms and rates available so you can make an educated decision.

Principal & Interest or Interest Only Options

We offer Home Equity Lines of Credit in both Principal and Interest (P&I) and Interest-Only (IO) options. Here’s a brief explanation of each. Your banker can help you decide which option is best for your financial goals.

Principal & Interest:

The draw period for P&I is 10 years, and during the draw period a portion of your monthly payment goes towards paying down principal while the other portion goes towards paying down accrued interest.

Interest Only:

The draw period for this HELOC is 5 years, and during the draw period your payments will only cover accrued monthly interest.

After the initial draw period, both HELOCs have a 15-year repayment period where you will be required to make principal and interest payments amortized to pay off the remaining balance in 15 years.

If you have any questions about our resources, tools or products, please contact us:

Speak to one of our knowledgeable product specialists to get answers or open account.

855-202-8731

Visit one of our banking center locations or schedule an appointment with a banker.